Is Our Project Allowable?

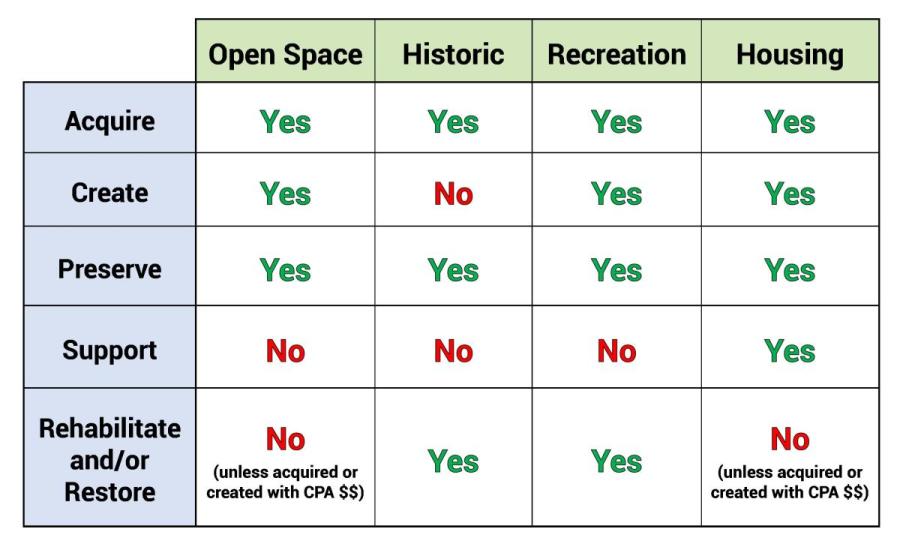

The chart below demonstrates the allowable uses of CPA funds in each of the CPA project categories: open space, recreation, housing, and historic preservation. This chart is critical for determining whether a proposed project is eligible for CPA funding. View a pdf version of the official Department of Revenue allowable uses chart.

Projects are only eligible for CPA funding if they fit in a box with a green "Yes" in the chart below (chart adapted from "Recent Developments in Municipal Law", Massachusetts Department of Revenue, October 2012):

A Deeper Look into CPA’s Project Categories

The CPA requires that communities spend, or set aside for future spending, a minimum of 10% of their annual CPA revenues for each of the three following categories: open space/recreation, historic preservation, and community housing. The remaining 70% of the funds are undesignated, and can be used for any allowable project in any of the CPA categories. This gives each community tremendous flexibility to determine its own priorities. Read on for a general overview of each of these categories; a decision on the allowability of specific projects in each community is determined locally by municipal counsel.

Open Space

Historic Preservation

Community Housing

Recreation

Open Space

Section 2 of the CPA legislation defines open space. It includes, but is not limited to, the following:

Section 2 of the CPA legislation defines open space. It includes, but is not limited to, the following:

- Land to protect existing and future well fields

- Aquifers, recharge areas, and watershed land

- Agricultural land

- Grasslands, fields and forest land

- Fresh and salt water marshes and other wetlands

- Ocean, river, stream, lake and pond frontage

- Beaches, dunes, and other coastal lands

- Lands to protect scenic vistas

- Land for wildlife or nature preserve

- Land for recreational use (see separate category information, below)

CPA funds may be spent on the acquisition, creation, and preservation of open space, and for the rehabilitation or restoration of any open space that has been acquired or created using CPA funds. It is important to note that a permanent deed restriction is required for all real property interests acquired under CPA. This restriction must be filed as a separate instrument, such as a Conservation Restriction (CR) or Agricultural Preservation Restriction (APR), and until this step has been completed, the terms of the CPA acquisition have not been technically fulfilled. Learn more about CRs.

Historic Preservation

Section 2 of the CPA legislation defines historic resources, preservation, and rehabilitation. Under CPA, an historic resource is defined as a building, structure, vessel, real property, document or artifact that is either:

Section 2 of the CPA legislation defines historic resources, preservation, and rehabilitation. Under CPA, an historic resource is defined as a building, structure, vessel, real property, document or artifact that is either:

- listed on the State Register of Historic Places; or

- determined by the local Historic Commission to be significant in the history, archeology, architecture, or culture of the city or town.

CPA funds may be spent on the acquisition, preservation, rehabilitation and restoration of historic resources. Communities using CPA funds on historic resources must adhere to the United States Secretary of the Interior's Standards for the Treatment of Historic Properties.

For more information, this flow chart details the steps to determining whether your historic preservation project qualifies for CPA funding. You can also read our technical assistance article, Which Historic Projects Qualify for CPA Funding?

Community Housing

Section 2 of CPA defines community housing.

The United States Department of Housing and Urban Development (HUD) income guidelines are used to determine who is eligible to live in the affordable housing units developed by communities with their CPA funds. Housing developed with CPA funds may be offered to those persons and families whose annual income is less than 100 percent of the areawide median income, as determined by HUD. See these figures for your community.

The United States Department of Housing and Urban Development (HUD) income guidelines are used to determine who is eligible to live in the affordable housing units developed by communities with their CPA funds. Housing developed with CPA funds may be offered to those persons and families whose annual income is less than 100 percent of the areawide median income, as determined by HUD. See these figures for your community.

Please note, though, that communities may choose to limit certain housing units created with CPA funds to those persons and families earning less than 80 percent of the areawide median income annually, as determined by HUD. This allows communities to include these units on their Subsidized Housing Inventory (SHI) with the state. See what those figures would be in your community.

CPA funds may be spent on the acquisition, creation, preservation and support of community housing, and for the rehabilitation or restoration of community housing that has been acquired or created using CPA funds. The CPA requires that whenever possible, preference be given to the adaptive reuse of existing buildings or construction of new buildings on previously developed sites.

Land For Recreational Use (Outdoor Recreation)

Section 2 also defines recreational use. The focus for CPA recreational projects is on outdoor passive or active recreation, such as (but not limited to) the use of land for:

- Community gardens

- Trails

- Noncommercial youth and adult sports

- Parks, playgrounds or athletic fields

CPA funds may not be spent on ordinary maintenance or annual operating expenses; only capital improvements are allowed. In addition, CPA funds may not be used for horse or dog racing facilities, or for a stadium, gymnasium, or similar structure. This prohibition has generally been interpreted to mean that CPA funds may be used only for outdoor, land-based recreational uses and facilities.

CPA funds may not be spent on ordinary maintenance or annual operating expenses; only capital improvements are allowed. In addition, CPA funds may not be used for horse or dog racing facilities, or for a stadium, gymnasium, or similar structure. This prohibition has generally been interpreted to mean that CPA funds may be used only for outdoor, land-based recreational uses and facilities.

CPA funds may be used for the acquisition of land to be used for recreation, or for the creation of new recreational facilities on land a community already owns. A 2012 amendment to CPA broadened the law to also allow for the rehabilitation of existing, outdoor recreational facilities. The amendment made it clear that with respect to land for recreational use, "rehabilitation" could include the replacement of playground equipment and other capital improvements to the land or the facilities thereon to make them more functional for their intended recreational use.

Another change ushered in by the 2012 amendment was a prohibition on the use of CPA funds for the acquisition of artificial turf for athletic fields. Communities may still use their CPA funds for other aspects of a field project, but must appropriate non-CPA funds to acquire the artificial turf surface.

Oct. 2012